The Elephant in the Room With CORSIA and Corresponding Adjustments

Overview

The Article 6 news out of COP29 was fantastic and we should all now push on.

However, the World Bank (https://lnkd.in/e8KFYeuH) has provided a “heads-up”.The provision of Corresponding Adjustment under Article 6 of the Paris Agreement is a crucial factor to consider when a country decides to participate in international carbon markets.

When the host country transfers authorised emission reduction credits (ETRs) or internationally transferred mitigation outcomes (ITMOs), a Corresponding Adjustment establishes an obligation and associated liability for the host country. Specifically, the host country is required to increase its Nationally Determined Contribution (NDC) burden by the volume transferred.

Without informed decision-making, countries may overstate their emission reduction potential and subsequently face the necessity of implementing more costly mitigation activities to meet their NDC commitments.

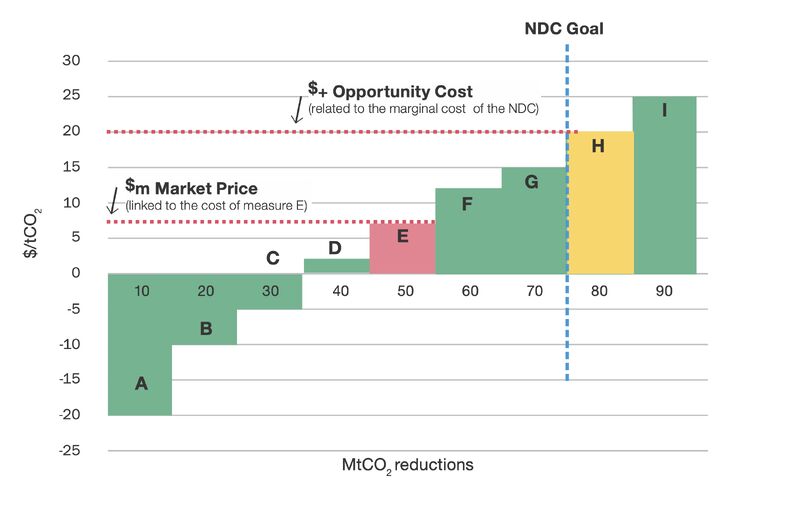

When a host country sells a carbon credit for a certain volume, additional emission reduction needs to accrue, creating an opportunity cost for the sale.For instance, a private project developer in a host country could reduce emissions at $7/tCO2e, but implementing an additional mitigation activity elsewhere in the economy to meet the host country’s emissions target might cost $20/tCO2e. Conversely, the developer could sell its emission reduction for as low as $7/tCO2e.

The country would need to pay $20/tCO2e to meet its NDC. See the World Bank chart below showing an example of opportunity cost of selling 10 MtCO2e at $7/tCO2e.In short, when a country sells/transfers an ITMO or correspondingly adjusted ETR it should do so knowing the marginal cost of abatement and that cost should be baked into the cost of the transfer.

That cost is different by nation. Over to you Lev Gantly and Greg Murray.